You're ready to jump into the housing market, but the thought of waiting weeks for mortgage approval is frustrating when you've found a home you want. Same-day pre-approval is real. But it only happens when your documents are ready before you apply and your lender has a process built for speed. Here's how to set yourself up for it.

What Pre-Approval Actually Means

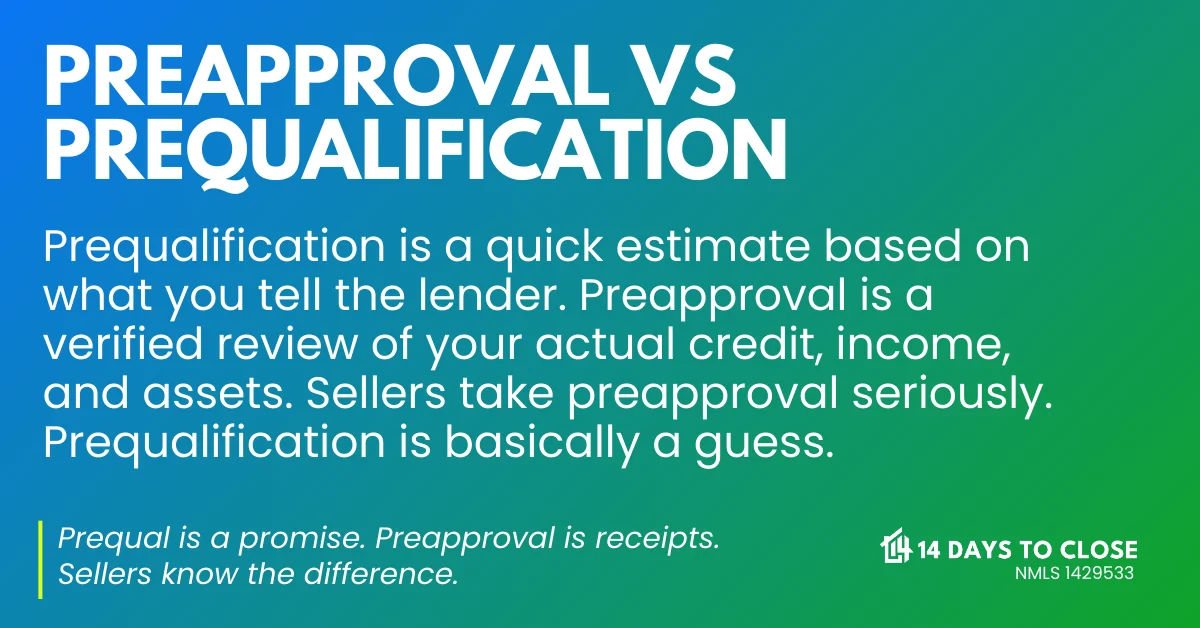

Mortgage pre-approval is a lender's formal statement that, based on a review of your financials, you're qualified to borrow up to a specific amount. It's more than a soft estimate. It shows sellers you're a serious buyer who's already cleared the first financial hurdle. In a competitive market, that matters. A seller choosing between two similar offers will almost always favor the one backed by a pre-approval letter.

The strongest version of this is a DU approval, a Desktop Underwriter approval that runs your file through automated underwriting. It gives sellers even more confidence than a standard pre-approval because it's closer to a full underwriting decision.

How to Make Same-Day Pre-Approval Happen

The buyers who get pre-approved fastest are the ones who show up prepared. Lenders aren't slow by default. They're slow when they're waiting for documents. If you submit a complete file the first time, you remove the back-and-forth that stretches timelines.

Gather these before you apply: recent pay stubs, bank statements from the last two months, the last two years of tax returns, proof of any additional income, and details on existing monthly debts. If you're self-employed, add profit-and-loss statements and two years of 1099s.

Ready to get pre-approved today?

Start your application now. If your file is complete, we can often turn a pre-approval the same day.

Your credit score is the other key variable. Check it before you apply. If it's lower than you'd like, ask your lender what programs fit your profile. There are solid options at a range of score levels. Knowing your number upfront means you don't get surprised partway through the process.

Can You Really Get Pre-Approved in One Day?

Yes, when your paperwork is ready and your lender uses digital processing tools. The system runs a credit check, your documents are reviewed, and a pre-approval letter is issued. The part that slows most people down is missing documentation: a bank statement from two months ago instead of the current one, a missing W-2, or an income source that wasn't accounted for. Those gaps create requests, and requests create delays.

Once you have your pre-approval, treat it carefully. Avoid opening new credit accounts or making large purchases. Keep your employment stable. Most pre-approvals are valid for 60 to 90 days. Lenders re-verify your financial status closer to closing, so any changes in that window can affect the outcome. More on how lenders verify your finances during the approval process.

Why Same-Day Pre-Approval Matters in a Competitive Market

In a bidding situation, having your pre-approval letter in hand when you submit an offer is a real advantage. Sellers see it as a sign that your deal is more likely to close on time. It's also practical: knowing your exact budget before you tour homes keeps you from falling in love with something you can't finance.

At 14 Days To Close, we've built our intake process to move fast. If you come in organized, we can get you pre-approved quickly and have a letter ready when you need it. Give us a call or start your application online. We're available nights and weekends.