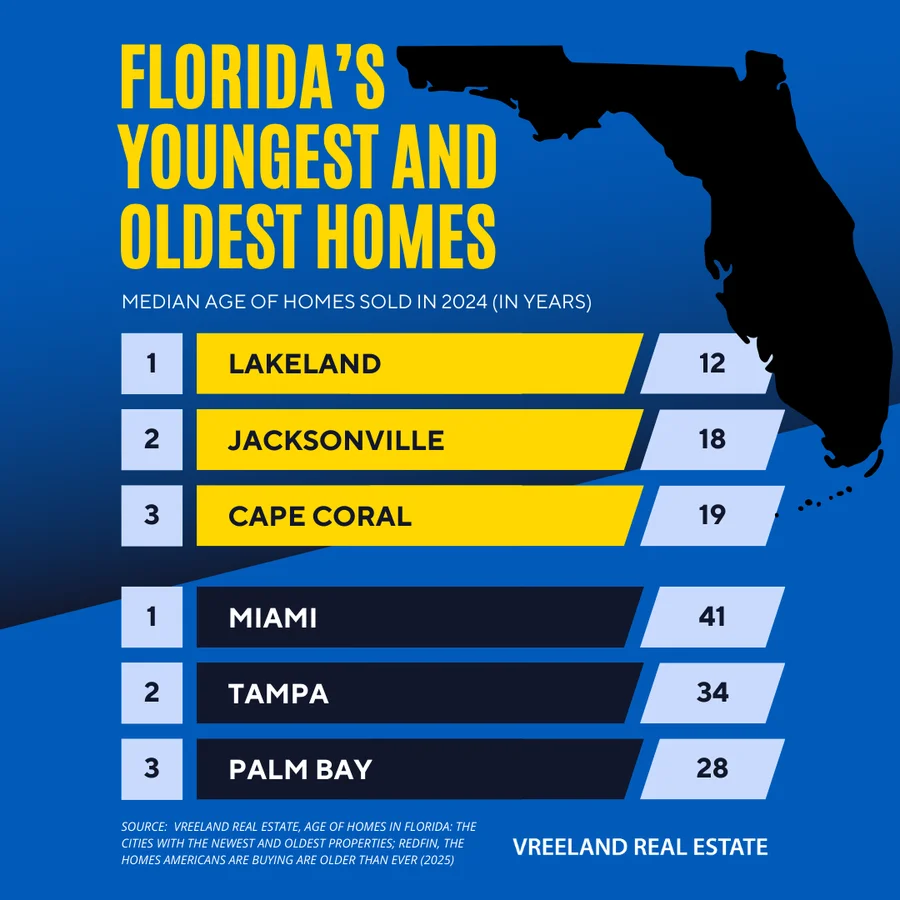

Florida's housing market is a time capsule. The median U.S. home sold in 2024 is a historic 36 years old, but the median age of Florida homes is 28 years, which means most were built in the late '90s. On one end, you've got brand-new communities in Lakeland and Cape Coral popping up faster than Publix subs. On the other, Miami's older homes are practically relics. Lenders treat these two extremes very differently, and that gap can shape everything from your appraisal to your insurance premium.

The Appraisal Tug-of-War

In Florida, new homes often get the red-carpet treatment during appraisals. Take Lakeland, where over 40% of homes sold last year were built after 2019. Appraisers favor these properties because they meet modern building codes, include energy-efficient features, and come with warranties that promise no surprise repairs. Lenders breathe easier knowing the roof won't leak and the AC won't quit, which means fewer hurdles to loan approval.

Older homes are a different story. In Miami, where two-thirds of homes sold are 30+ years old, appraisers play detective. That 1990s gem might have "good bones," but outdated electrical systems or aging plumbing can trigger repair requirements. A Jacksonville home built in the '90s might appraise for $300,000, which is $100,000 less than a comparable new build, but the lender could demand a $15,000 roof replacement before signing off. Suddenly, that "bargain" isn't so simple.

Builder Incentives vs. Renovation Loans

Builders frequently partner with lenders to offer rate discounts, closing cost credits, or free upgrades. These perks make loans easier to approve because lenders trust the builder's reputation and the newness of the property.

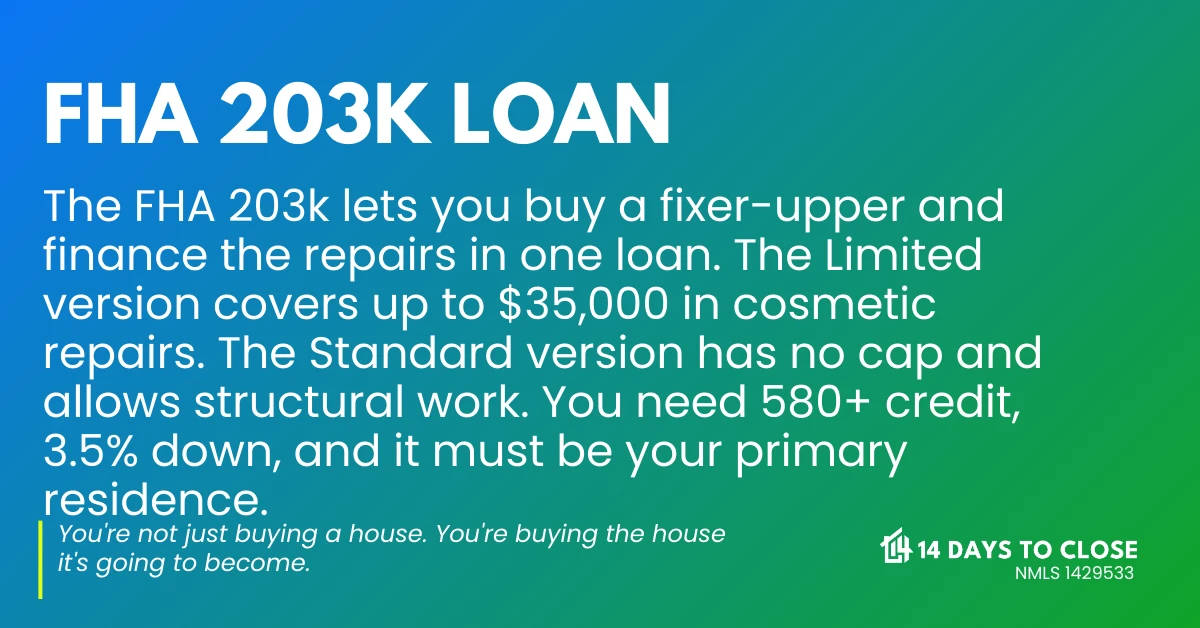

If you're eyeing a classic Florida home, you may need a renovation loan instead. In Orlando, where older homes sell for around $335,000 compared to $446,000 for new builds, buyers often turn to FHA 203(k) loans to bundle purchase and repair costs. The catch: you'll need contractor bids and a lender who believes in your vision. It's a legitimate path, but don't expect a quick close on a renovation loan.

Wondering if going with your builder's lender is the right move? Our breakdown of builder loans vs. bank loans walks through what to consider before you commit.

Not sure which loan fits your Florida home?

New build or older home, we'll tell you exactly what to expect from the approval process before you make an offer.

Start My Pre-ApprovalInsurance: The Hidden Approval Variable

Insurers charge more for older homes, especially near the coast. A new build in Palm Bay might have impact-resistant windows and a fortified roof, trimming your premium to $3,500 per year. Lenders see that as a green light.

In Miami, insuring a 30-year-old home can cost $5,000 or more annually, if you can find coverage at all. Outdated wiring or a worn roof may spook insurers, and lenders can respond by slashing your approved loan amount or demanding extra cash upfront. Insurance isn't just a monthly bill. It's an approval factor.

Where New Construction Has the Edge

Cities like Lakeland and North Port have room to sprawl, so builders have been pumping out inventory. That supply means lenders in these markets are pros at handling construction loans and offering extended rate locks if your build runs late.

In land-crunched markets like Tampa or Miami, older homes dominate. Lenders in these areas are used to appraisals that hinge on location over condition. A 1980s bungalow in Tampa's Hyde Park might sail through approval because of its walkable neighborhood, even if it needs a kitchen overhaul. Location can offset age, but only up to a point.

What This Means for Your Approval Strategy

New homes mean smoother approvals, builder perks, and lower insurance. Older homes mean lower prices, renovation loan options, and location advantages, but prepare for appraisal surprises and insurance complications. With 28 years being the median age of a Florida home sold last year, most buyers will face at least one of these trade-offs.

The key is knowing which hurdles are in front of you before you're under contract. If you're comparing a new build to a 1990s home and want to know how each would play out with a lender, read about what kills deals at the last minute and call us to run the numbers on both.