Florida homeowners add pools, outdoor kitchens, bonus rooms, and ADUs (accessory dwelling units) at a higher rate than almost any other state. The financing for these projects follows a set of options that differ significantly from home purchase financing. Here's what works and what costs the most over time.

Cash-Out Refinance

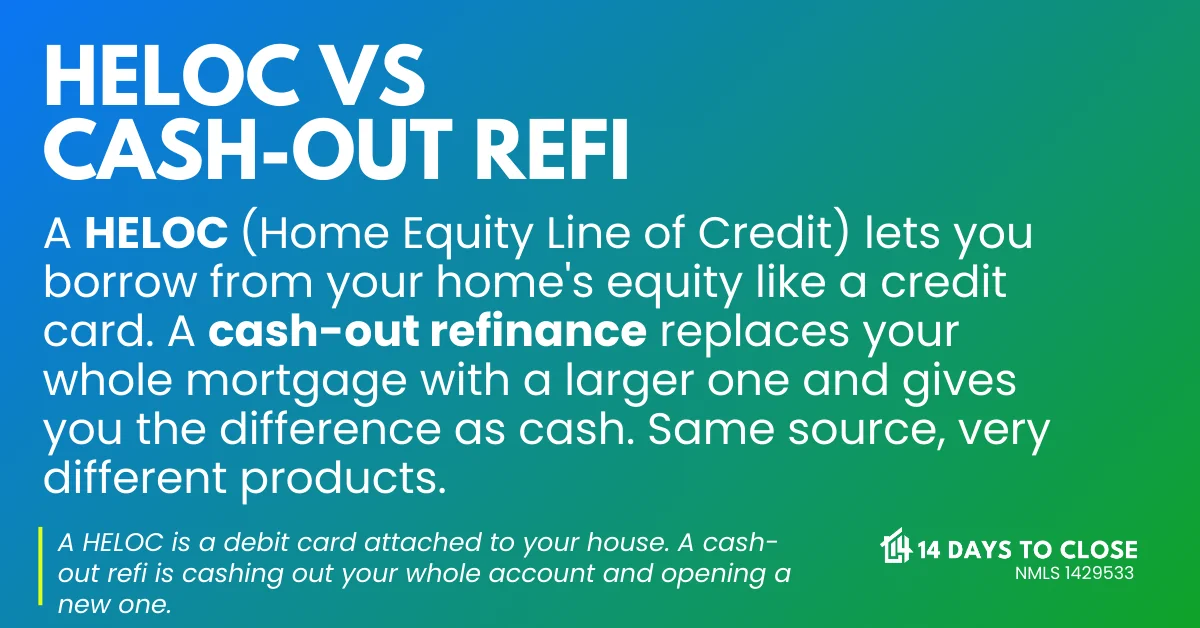

A cash-out refinance replaces your existing mortgage with a new, larger mortgage and gives you the difference in cash. If your home is worth $500,000 and you owe $280,000, you have significant equity to access. Conventional guidelines allow cash-out up to 80 percent of the appraised value.

The advantage: mortgage rates, even for cash-out refinances, are typically the lowest available financing for home improvements. You're replacing a high-rate financing option with a lower-rate mortgage. The disadvantage: you're resetting your mortgage term and potentially giving up a low existing rate. If you locked a 3.5% rate in 2021, refinancing in 2026 at a higher rate to pull cash out might not pencil out even if the pool itself is a worthwhile investment. See our guide to cash-out refinance vs. HELOC to compare the two options side by side.

HELOC: Home Equity Line of Credit

A HELOC lets you borrow against your equity as a revolving line of credit, similar to a credit card, but secured by your home. You draw funds as needed during the draw period (usually ten years), pay interest on what you've borrowed, and repay the balance over the repayment period.

For phased projects, like building a pool that takes six to eight months with multiple contractor draws, a HELOC's flexibility has real value. You pay interest only on what you've drawn, not the full line amount. HELOC rates are typically variable and tied to the prime rate. They're generally higher than mortgage rates but lower than personal loans or credit cards.

Home Equity Loan

A home equity loan is a second mortgage in a fixed amount at a fixed rate. You receive the full amount at closing and repay it over a set term. This works well for a defined project with a known cost: a pool at $55,000, for example, where you know the total upfront.

Rates are typically a percentage point or two higher than primary mortgage rates, but the certainty of a fixed payment has real value when you're already carrying a primary mortgage. For a project with a defined scope and budget, the home equity loan structure is often cleaner than a HELOC.

FHA 203(k) or Fannie Mae HomeStyle Renovation Loans

If you're buying a home and planning improvements simultaneously, renovation financing wraps the purchase and renovation cost into one mortgage. FHA 203(k) and Fannie Mae's HomeStyle loan both work this way. The loan is based on the after-improved value of the property, which can cover projects that would otherwise exceed your available equity.

Cash-Out vs HELOC: Which One Costs Less for Your Project?

The right answer depends on your current rate, your equity, and your project timeline. We'll run the comparison and show you which option costs less over the life of the financing.

For existing homeowners, these products are available as refinances, but they require the project to be completed by a licensed contractor and go through a specific draw process. They're more complex than a HELOC but offer better rates for buyers who need to combine purchase and renovation financing in one loan.

Pool-Specific Financing

Pool contractors often offer financing through lending partners. The rates are almost always higher than home equity financing, but the process is faster and doesn't require tapping home equity. For homeowners with limited equity but strong income, this can be a practical path to move forward quickly.

Compare the total interest cost over the loan's life against the equity-based options. A $50,000 pool financed through a contractor at 11% over ten years costs dramatically more than the same amount at 8% through a HELOC. Run the actual numbers before you sign with the contractor's lender.

Florida Permit Requirements

Florida requires permits for pools, structural additions, and many home improvements. Work done without permits can complicate a future refinance or sale when the appraiser or lender flags unpermitted improvements. Always confirm your contractor is pulling the appropriate permits before work begins.

At 14 Days To Close, we work with homeowners on cash-out refinances, HELOCs, and home equity loans for improvement projects across Florida. Give us a call or start your application to see what your equity makes possible.