Your home isn't just where your heart is. It's also packed with real financial potential. When you're ready to tap into that value, you've got two big options: a cash-out refinance or a HELOC. Think of it like choosing between power tools. Both get the job done, but the right one depends on what you're building.

What Is a Cash-Out Refinance (and Should You Do It)?

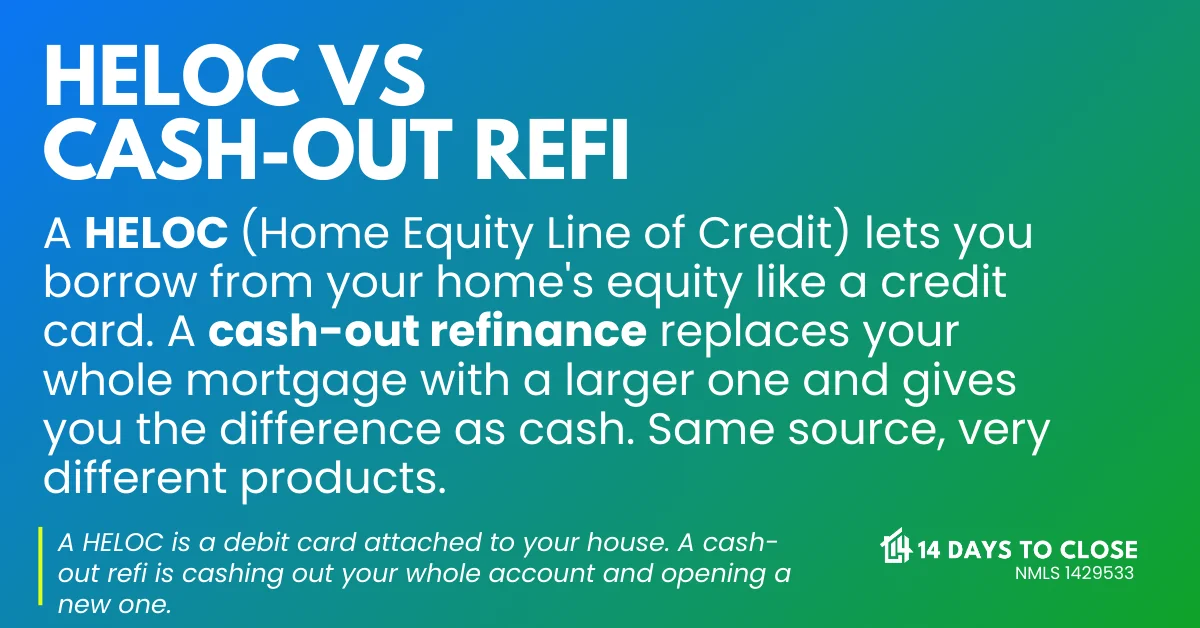

A cash-out refinance is like giving your mortgage a makeover, with a payout. You take out a new loan for more than you currently owe, use it to pay off your old one, and pocket the extra cash.

People usually tap into this option for big goals: renovating a kitchen, consolidating high-interest debt, or funding major life moves. One of the perks? Fixed interest rates. That means predictable monthly payments, which is great if you're planning long-term.

If today's rates are lower than what you locked in years ago, it could be a win-win. You walk away with cash in hand and potentially lower interest. Just watch for closing costs, which typically fall between 2 to 5% of the loan. And remember, your mortgage clock resets.

What Is a HELOC (and When Does It Make Sense)?

A HELOC, or Home Equity Line of Credit, works a lot like a credit card, except your home is on the line. You get a revolving line of credit based on your home's equity, and you can borrow from it as needed during the draw period, usually about 10 years.

You only pay interest on what you actually use, which makes it a flexible option for ongoing or unpredictable expenses. Think multi-phase renovations, medical bills, or emergency backups you hope you never need.

Unlike cash-out refinances, HELOCs usually come with variable interest rates. That means your payments can change over time, depending on market conditions. This flexibility is a big plus, but it also comes with risk, especially if rates climb.

Not Sure Which Option Fits Your Situation?

Our loan team can walk through the numbers on both, so you leave the conversation knowing exactly which path makes sense for your goals.

Which Is Better for Home Renovations?

Cash-out refinances usually come with lower, fixed interest rates. HELOCs often start lower as well, but those rates can shift over time since they're variable.

If you're planning a big, one-time project like a $50,000 kitchen remodel, the steady rate of a cash-out refi can offer peace of mind and long-term savings. You know exactly what your payment will be every month.

If you're handling smaller upgrades over time, such as landscaping or outdoor improvements in phases, a HELOC gives you more flexibility. You only borrow what you need, when you need it.

Thinking about consolidating debt with home equity? A cash-out refi can streamline multiple payments into one. Just know that if your HELOC rate jumps mid-project, your plan can unravel fast. Both options put your home on the line, so make sure the numbers work before you commit.

Credit Score Considerations

HELOCs are often easier to qualify for if your credit is in the middle range. But easier access usually means higher interest rates, so you pay for that flexibility.

Cash-out refis require stronger credit and a lower debt-to-income ratio, but they can reward you with lower monthly payments and better long-term terms if you qualify. Knowing your credit profile is the starting point for this decision, and it's worth talking through before you apply for either.