Finding the right mortgage can feel like a lot. Conventional loans are one of the most common options, and they come with genuine advantages, plus a few real drawbacks. Since they're not backed by the government the way FHA loans are, the rules work a bit differently. You'll typically need a higher credit score, but the trade-off can be better interest rates and more flexibility in how you structure the loan.

You can use a conventional loan for your main home, a second home, or even a rental property. That range of options makes them appealing to buyers in a lot of different situations. Here's a clear look at the highlights, pros, and cons so you can figure out if conventional financing fits your goals.

What Is a Conventional Loan?

A conventional loan is a standard mortgage that isn't backed by any government agency like the FHA or VA. These loans come from private lenders, and each lender sets its own qualifying criteria based on your financial picture. You'll generally need a credit score of at least 620, and the better your credit and income, the stronger your approval terms will be.

What sets conventional loans apart: no government insurance is involved, a higher credit score is usually required, and they can be used for a wide range of property types. That includes your primary home, a vacation property, or an investment property.

Highlights at a Glance

Conventional loans come with features that make them a solid fit for many buyers. If your credit is strong, you'll likely qualify for a lower interest rate, which adds up to real savings over the life of the loan. You also get the ability to pick between fixed-rate and adjustable-rate terms depending on your situation and comfort level.

Key highlights include lower interest rates for buyers with strong credit, flexible terms with fixed or adjustable options, the ability to borrow up to the conforming loan limit, and PMI that can be removed once you reach 20% equity. That last one matters a lot compared to FHA, where mortgage insurance typically sticks around much longer.

The Real Pros of Conventional Loans

There are concrete advantages here, especially if your finances are solid. One of the biggest is the potential for lower overall borrowing costs. If your credit score is high, you'll likely qualify for better interest rates and loan terms than you'd get with a government-backed loan.

These loans are also flexible when it comes to property types. You can buy a house, condo, or even a multi-unit building. Unlike FHA loans, you don't pay upfront mortgage insurance. If you put down at least 20%, you skip PMI entirely. And if you put down less, you can cancel PMI later once you hit that 20% equity mark.

The Real Cons of Conventional Loans

Conventional loans aren't the right fit for every buyer. They can be harder to qualify for, especially if your credit score needs work or you don't have much saved for a down payment.

You'll typically need a score of at least 620, and while you might be able to put down as little as 3%, many buyers end up putting down more to avoid the added monthly cost of PMI. If you're under 20%, PMI sticks around until you build enough equity. The underwriting process also involves stricter income and financial checks than government-backed programs. If you're a self-employed buyer or have variable income, alternative income loan options might be worth reviewing alongside conventional.

Compare Your Options Before Deciding

FHA or conventional? The right answer depends on your credit, down payment, and long-term goals. We'll run the numbers on both and show you what actually saves you more.

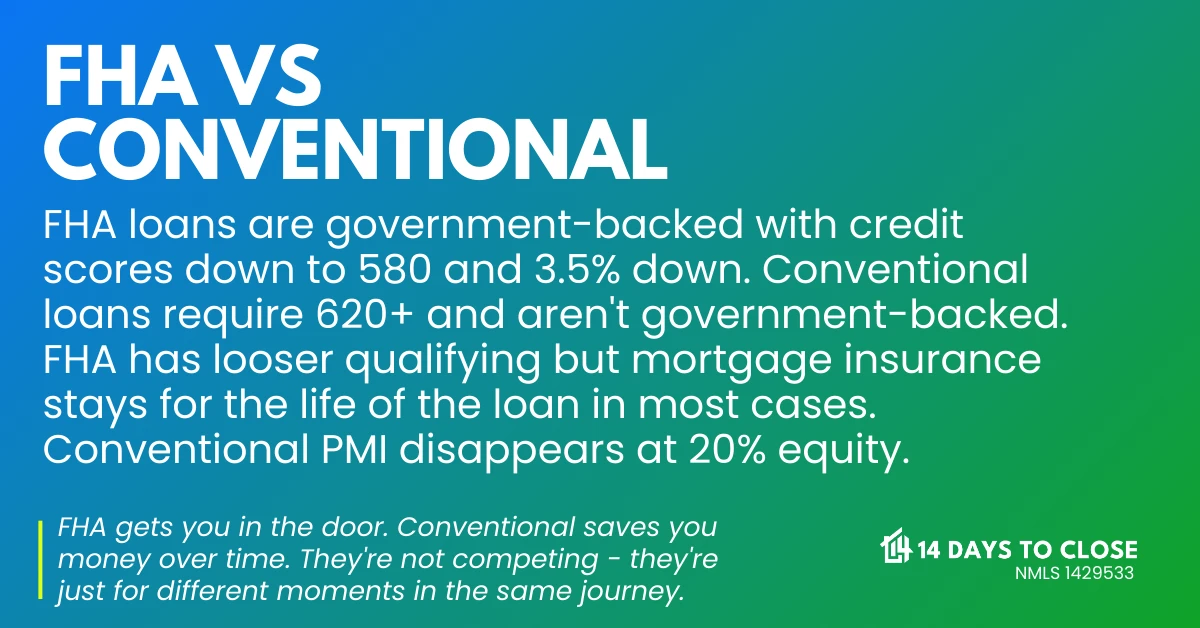

Conventional vs. FHA: Key Differences

Conventional and FHA loans work differently, and understanding those differences helps you figure out which fits your situation better. Conventional loans are stricter on credit but reward strong financial profiles with better rates and fewer long-term costs. FHA loans are more forgiving on credit and down payment requirements, but mortgage insurance sticks around longer.

| Factor | Conventional Loan | FHA Loan |

|---|---|---|

| Credit Score | 620+ | 580+ |

| Down Payment | As low as 3% | 3.5% minimum |

| Mortgage Insurance | PMI if under 20%, removable | Required for most loans, longer term |

| Property Use | Primary, second home, or investment | Primary residences only |

Who Should Look at Conventional Financing?

Conventional loans are a strong option if your credit score is solid and your income is stable. If you can put down 20%, you'll skip PMI and likely lock in a competitive rate. They're also the right call if you want to buy a second home or an investment property, since FHA programs don't allow that.

You might be a good fit if you have a credit score of 620 or higher, can manage a meaningful down payment, want to avoid long-term mortgage insurance, need flexibility on property types, or prefer more control over your loan terms.

Is Conventional Right for You?

It comes down to your financial situation and goals. If you have solid credit, steady income, and enough saved for a down payment, conventional financing can give you more options and lower long-term costs. Not sure what fits? Give us a call or schedule a time to talk and we'll walk you through both options based on your actual numbers.