Financing a condo in Florida isn't just about qualifying as a buyer. The building itself has to qualify too, and in Florida's condo market right now, that's the part that catches people off guard. A lot of buildings that were financeable two years ago are no longer approved for FHA or conventional loans.

Why Condo Financing Is Different

When you buy a single-family home, the lender evaluates you. When you buy a condo, the lender evaluates both you and the condo association. They want to know: is the HOA financially healthy? What percentage of units are owner-occupied? Are there any pending lawsuits? Is the reserve fund adequate?

If the building fails any of those tests, you can't get conventional or FHA financing there, regardless of how strong your application is. You'd need to pay cash or use a portfolio lender who doesn't sell loans to Fannie or Freddie. For a broader look at how these agency guidelines work, see our overview of conventional loan requirements.

FHA Condo Approval in Florida

FHA has a list of approved condo projects. The list is searchable through HUD's website, but it changes frequently. Florida's condo market has seen a significant number of buildings lose FHA approval or fail to renew it since the Surfside collapse in 2021 led to new reserve requirements under Senate Bill 4D.

If the building isn't on the approved list, FHA has a Single-Unit Approval process that allows individual units to be financed even in non-approved buildings. It's more documentation-intensive, but it works for many buyers.

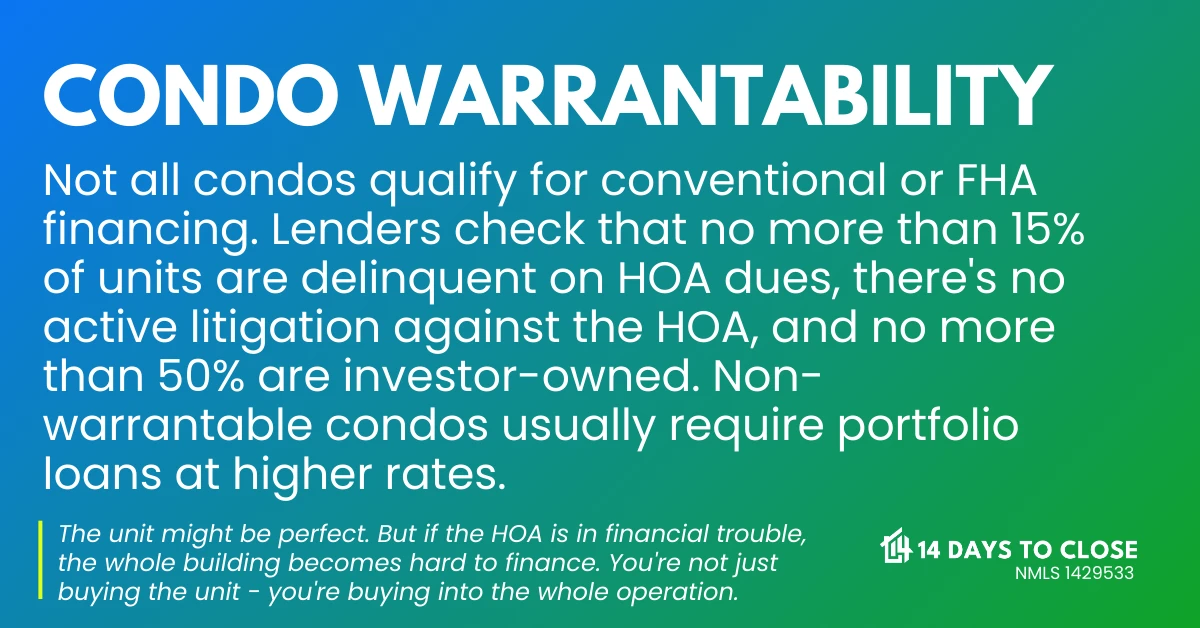

Conventional Financing and Warrantable Condos

For conventional loans, Fannie Mae and Freddie Mac require the condo to be "warrantable." That means the HOA meets specific criteria: less than 35% of units are rentals, no single entity owns more than 10% of the units, the project isn't in litigation, and the association is adequately funded.

Non-warrantable condos can still be financed, but you'll need a non-QM or portfolio lender, which typically means a higher rate and a larger down payment. See our guide to FHA loan limits in Florida for additional context on how FHA program rules affect condo purchases.

Not Sure If Your Building Qualifies?

Tell us the address and we'll find out what your financing options are, including non-warrantable solutions if the building doesn't meet standard requirements.

Check My Condo OptionsWhat to Check Before Making an Offer

Ask the listing agent for the condo questionnaire and the most recent HOA financials. If the association can't or won't provide them, that's a red flag. Your lender will need these documents to determine financing viability, so getting them early saves everyone time.

If you're not sure where a building stands, talk to a mortgage broker before you make an offer. A few minutes of due diligence prevents a lot of problems. At 14 Days To Close, we deal with Florida condo financing regularly, including non-warrantable buildings and buildings with FHA approval issues.