You found the investment property. The numbers work, you're ready to move, and you want the asset held in your LLC. When you call most lenders about a conventional loan under the LLC, the answer is no. Conventional lenders aren't being difficult. They're following rules set by Fannie Mae and Freddie Mac, which require that borrowers be natural persons, not entities.

But investors work around this every day. There are two legitimate paths, and knowing which one applies to your situation is the difference between closing and stalling.

Why Conventional Lenders Won't Write Directly to an LLC

Most conventional loans are backed by Fannie Mae or Freddie Mac, two government-sponsored enterprises that set underwriting rules for loans sold on the secondary market. Both have a core requirement: the borrower must be a natural person, not an entity.

This isn't bureaucratic friction for its own sake. It's built into their credit scoring models, loan-level pricing adjustments, and indemnification requirements. When a loan is sold on the secondary market, the buyer of that loan wants to know exactly who they're lending to. An LLC can be dissolved, transferred, or have its ownership restructured without notice. A person is a relatively fixed concept for legal and underwriting purposes.

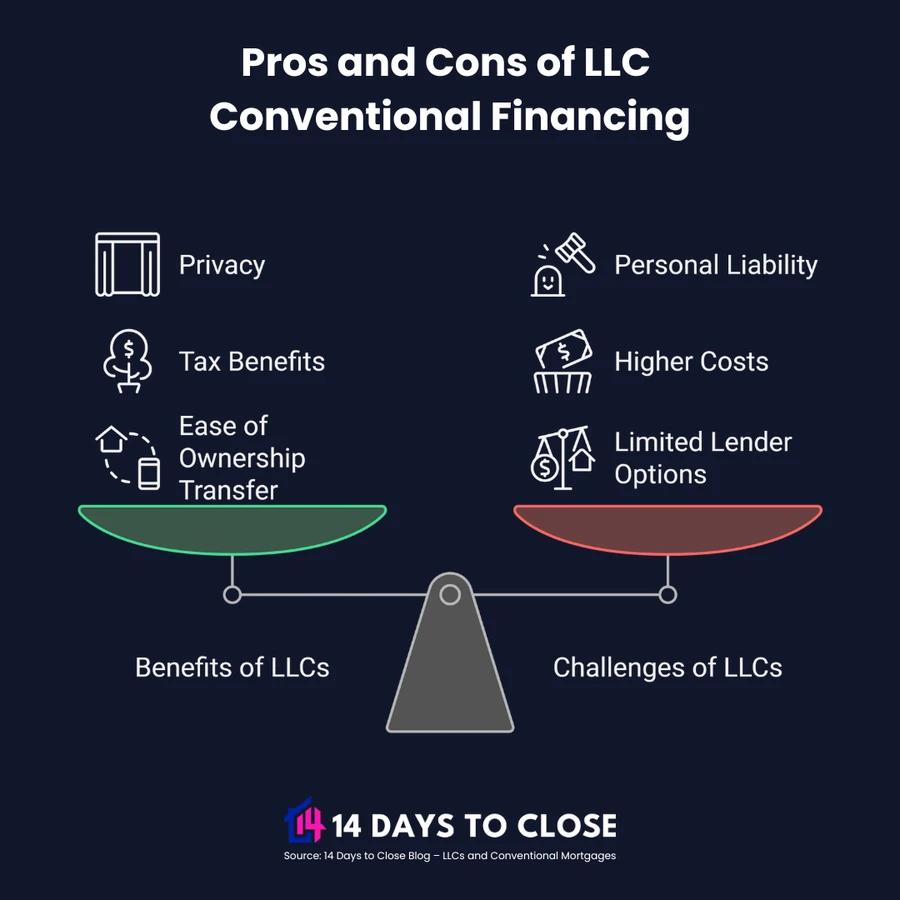

Fannie and Freddie also require personal liability recourse. In certain default scenarios, they want the ability to go after personal assets. An LLC limits recourse to the LLC's assets only, that's the whole point of using one, but it's not what conventional lenders can accept.

The Two Real Paths Investors Use

Path 1: Close in your personal name, then deed into the LLC after closing.

You get pre-approved and close the loan in your own name. After closing is complete and the deed is recorded, you transfer the property to your LLC by filing a new deed. The mortgage stays in your personal name. The property ownership changes.

Technically, this triggers the due-on-sale clause in your mortgage, a provision that lets the lender call the loan due if the property changes ownership. In practice, residential investment property lenders almost never enforce this on compliant, performing loans. They don't have the resources to monitor every property transfer. As long as you're making payments, they won't notice or act. This is the most common path investors take.

Path 2: DSCR loans, portfolio loans, or commercial financing directly in the LLC name.

DSCR (Debt Service Coverage Ratio) loans and portfolio loans are non-conforming products that lenders keep in-house rather than selling to Fannie or Freddie. Because they don't sell to the secondary market, they can write to entities directly. The underwriting is based on the property's income potential, not your personal income, which works well for investors managing multiple properties.

DSCR loans typically require a 20-25% down payment, carry slightly higher rates than conforming conventional loans, and don't use personal income in qualification. For many investors, this is actually the preferred path, cleaner ownership from the start, no due-on-sale risk.

Why Investors Set Up LLCs in the First Place

Before deciding which financing path to use, it's worth understanding what the LLC actually does for you.

- Asset protection: If a tenant sues over a property issue, the lawsuit is filed against the LLC, not against you personally. Your personal assets are separated from the lawsuit.

- Ownership transfer: Selling or transferring ownership of the LLC's membership interests can be simpler than re-titling real estate.

- Estate planning: LLC membership interests can be structured for estate planning purposes more easily than individual property deeds.

- Privacy: The property records show the LLC as owner, not your personal name.

The protection only works if you maintain proper separation between your personal finances and the LLC's. Commingling funds, signing personal guarantees without tracking them, or failing to treat the LLC as a real entity can pierce the corporate veil and eliminate the protection.

What to Know Before You Start

Investing in Florida real estate through an LLC?

We can walk you through both paths and find the financing structure that closes fastest.

A few things to get clear before you start your application.

Lender selection matters. Not every lender offers DSCR or portfolio products. If you want LLC-direct financing, you need a lender who keeps loans in-house or specifically offers non-QM products. Most big retail banks won't have this.

Personal guarantee expectations. Even on LLC-direct loans, many lenders require a personal guarantee from the managing member. You're still on the hook personally, but the entity is the legal borrower.

Rate and term differences. DSCR loans carry higher rates than conforming conventional loans, typically 0.5% to 1.5% higher depending on credit, LTV, and the property's cash flow profile. Factor this into your return calculations.

Down payment requirements. DSCR loans usually require 20-25% down minimum. Conforming conventional investment property loans require 15-25% depending on the property type and lender.

At 14 Days To Close, we work with investors buying under LLCs and with personal names alike. If you're working through the structure of a deal and want to understand which path closes fastest for your specific situation, reach out below.