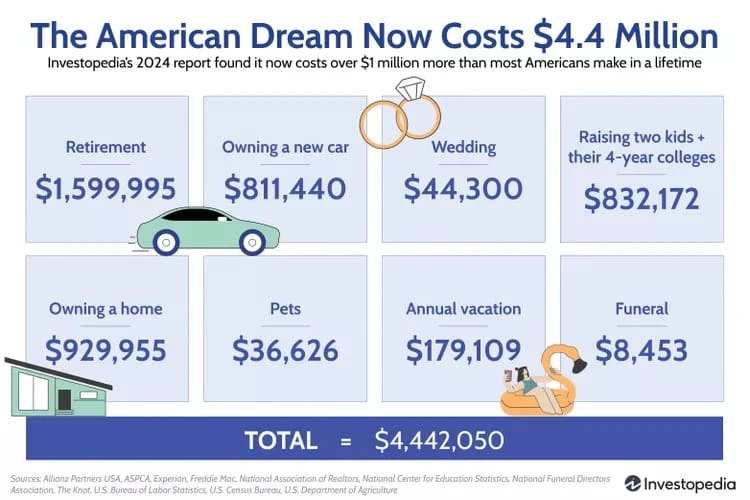

There's a conversation that happens at kitchen tables across America. Someone over 60 mentions what they paid for their first house. The number is something like $32,000. Or $41,000. Or if it was a coastal city, maybe $68,000. Then comes the advice: save more, spend less, cut back somewhere. The conversation ends. The problem doesn't.

This post is the math that gets left out. Not as an argument, but as context. The inputs changed. The comparison doesn't hold. Here's why.

The Price-to-Income Ratio Has Doubled

In 1975, the median U.S. home sold for $39,500. The median household income that year was $13,719. That's a ratio of roughly 2.9 times annual income to buy a home.

In 2024, the median U.S. home sold for approximately $420,000. Median household income sits at about $80,610. That's a ratio of 5.2 times annual income.

Prices didn't just go up. They went up nearly twice as fast as income over those 50 years. That's the structural shift. You can budget better and save more aggressively, but you can't save your way out of a ratio problem.

The Down Payment in Work Hours

Dollar amounts are easy to dismiss. Work hours are harder to argue with.

In 1975, the average U.S. hourly wage was approximately $6.60, per Bureau of Labor Statistics data. A 20% down payment on a $39,500 house was $7,900. At $6.60 an hour, that's roughly 1,197 hours of work, about 30 weeks of full-time employment.

In 2024, the average U.S. hourly wage is approximately $35.56. A 20% down payment on a $420,000 home is $84,000. At $35.56 an hour, that's 2,362 hours, or 59 weeks of full-time work.

That's before taxes. After a reasonable effective rate, you're looking at closer to 75 to 80 weeks of net take-home pay to hit that number. While paying rent the entire time.

| Item | 1975 | 2024 | Change in Work Hours |

|---|---|---|---|

| 20% down payment (median home) | ~1,197 hrs (30 wks) | ~2,362 hrs (59 wks gross) | +97% more work |

| One year of public university tuition | ~93 hrs (2.3 wks) | ~326 hrs (8.2 wks) | +251% more work |

| Average new vehicle | ~750 hrs (18.8 wks) | ~1,320 hrs (33 wks) | +76% more work |

| Annual employee health insurance premium | ~0 hrs (employer paid) | ~177 hrs per year | New cost entirely |

The 18% Rate Argument

This one comes up every time, so let's get through it.

In 1981, the average 30-year fixed mortgage rate peaked at 18.6%, per Freddie Mac data. That number is real and nobody's disputing it. But here's what the comparison leaves out.

In 1981, the median home price was around $70,000. A 30-year mortgage at 18.6% on $70,000 with 20% down runs about $875 a month. Today's 6.9% rate on a $420,000 home with 20% down is approximately $2,228 a month. The high-rate era still produced a lower monthly payment on a lower-priced asset.

The 1981 buyer also had one more advantage: rates dropped. Steadily, for the next four decades. When rates fell from 18% to 12% in the mid-1980s, those homeowners refinanced and cut their payments in half. The home didn't get more expensive. It got cheaper to carry. That's not a trick available to buyers who purchased at $420,000 with the expectation that rates would stay high.

What a Year of College Cost (In Work Hours)

Housing is the main event. Student loans are the opening act that your parents' savings timeline didn't have to account for.

In 1975, the average in-state tuition at a public four-year university was $617 per year, per the National Center for Education Statistics. At $6.60 an hour, that's 93 hours of work, about two and a half weeks. A summer job at minimum wage ($2.10 an hour) netted roughly $1,000 over 12 weeks. Covered tuition and left money on the table.

In 2024, the average in-state tuition at a public four-year university is $11,610 per year, per the College Board. At $35.56 an hour, that's 326 hours, about eight weeks of full-time work. At the federal minimum wage of $7.25 an hour, it's 1,601 hours. A summer job at minimum wage covers roughly one month of tuition at today's rates.

The buyers who are 28 to 38 years old right now didn't just face a more expensive housing market. They entered it carrying debt that their parents never had to factor into a savings plan.

Find Out What You Can Afford Right Now

The 20% down benchmark isn't a requirement. There are paths in at 3% to 3.5% down. A 20-minute call shows you exactly where you stand.

Three Budget Lines That Didn't Exist in 1975

This is the part that gets skipped in most affordability conversations, because it's harder to put on a chart. But these three costs either didn't exist or were negligible in 1975, and they're very real today.

Healthcare: In 1975, most employers covered the full premium. Employee out-of-pocket contributions were close to zero for most families. In 2024, the average employee contribution for employer-sponsored family health insurance is $6,296 per year, per the KFF Employer Health Benefits Survey. That's roughly $525 a month leaving the account before rent.

Childcare: Full-time center-based infant daycare averaged around $400 a month in the mid-1980s. In 2024, it averages $1,582 per month nationally, per the Economic Policy Institute, and runs over $2,000 in most major metro areas. In some cities it costs more than a mortgage. This was not a line item in 1975 household budgets the way it is today, because the cultural and economic expectation of dual-income households with full-time childcare didn't exist at the same scale.

Student loan payments: The median monthly student loan payment for borrowers in repayment is approximately $300. That's a monthly budget item that did not exist for most Boomer home buyers. It runs alongside rent, healthcare, childcare, and whatever's left to save.

When someone says "we saved for a house on one income," those three categories explain a lot of the math that's missing from the comparison.

Cars and Groceries

Both come up in these conversations, so it's worth being precise about where they land.

The average new vehicle cost roughly $4,950 in 1975, about 750 hours of work at average wages. In 2024, the average new vehicle transaction price is approximately $47,000, about 1,320 hours of work. Worse, but not in the same league as housing. Used cars are a sharper story: post-pandemic inventory disruptions pushed used vehicle prices to levels that made a reliable $8,000 commuter car harder to find than it had any right to be.

Groceries are a more complicated comparison. A gallon of milk cost $0.77 in 1975. It costs roughly $4.50 today. But average wages are also about five times higher. Most basic staples, rice, canned goods, produce, are roughly comparable in work-hour terms to 1975, and some goods like electronics, clothing, and packaged goods have gotten cheaper in real terms. The monthly grocery bill as a dollar amount is genuinely shocking. The work-hour equivalent is not where the structural problem lives.

The real issue isn't that every single thing costs more in terms of work time. It's that the items you can't substitute or skip, housing, education, healthcare, and childcare, cost dramatically more, and those four things are the ones that determine whether you build wealth or just break even.

What You Can Do With This Information

This post won't change how dinner table conversations go. But it gives you something more useful than frustration: a clearer picture of what the actual entry points are.

The 20% down payment benchmark your parents likely hit isn't a hard requirement. FHA loans close at 3.5% down. On a $420,000 home, that's $14,700 instead of $84,000. A different savings timeline entirely. Conventional loans have 3% options for qualifying first-time buyers.

Down payment assistance programs exist in most states and are genuinely underused, mostly because buyers don't know about them until someone mentions it. Florida has several worth knowing about before you assume you need the full amount. See what's currently available through Florida down payment assistance programs.

The number that matters most isn't the sticker price. It's what you qualify for and what you can carry month to month. Run the affordability calculator to get a payment estimate based on your income and down payment before you even talk to a lender. Then a 20-minute pre-qualification sharpens those numbers into something real. Before you decide the math is impossible, find out what you actually need saved for your specific situation.

The structural problem is real. It's also not unsolvable. Most buyers who close don't have 20% down. They have a plan that works on the numbers in front of them, not the ones from 1975.

Sources

- U.S. Census Bureau, American Housing Survey and Historical Census of Housing Tables: Median Home Sales Price, 1975 and historical series

- U.S. Census Bureau, Current Population Survey: Median Household Income, 1975 and 2023

- Bureau of Labor Statistics, Occupational Employment and Wage Statistics: Average Hourly Earnings, historical and current

- Freddie Mac, Primary Mortgage Market Survey: 30-Year Fixed Mortgage Rate Historical Data (1971-present)

- National Center for Education Statistics, Digest of Education Statistics: Average Undergraduate Tuition and Required Fees, Public Institutions (1975)

- College Board, Trends in College Pricing and Student Aid 2024: Average In-State Tuition, Public Four-Year Universities

- KFF (Kaiser Family Foundation), 2024 Employer Health Benefits Survey: Average Annual Worker Contribution, Family Coverage

- Economic Policy Institute, Child Care Costs in the United States (2024 Report): Average Monthly Cost, Center-Based Full-Time Infant Care

- National Association of Realtors, Existing-Home Sales Data: Median Sales Price, 2024

- Kelley Blue Book / Cox Automotive, Average Transaction Price Report: U.S. New Vehicles, 2024