Co-buying with friends has been a popular way to break into the housing market when prices are high and rates are punishing. But that approach is losing ground fast. According to a recent Zillow survey, the share of buyers purchasing a home with friends dropped from 14% in 2023 to just 7% in 2024, a 50% decline in one year.

The Federal Reserve's rate cuts are a major driver. As borrowing costs drop, individual buyers are finding it more realistic to buy on their own, and that changes the math entirely on co-buying arrangements.

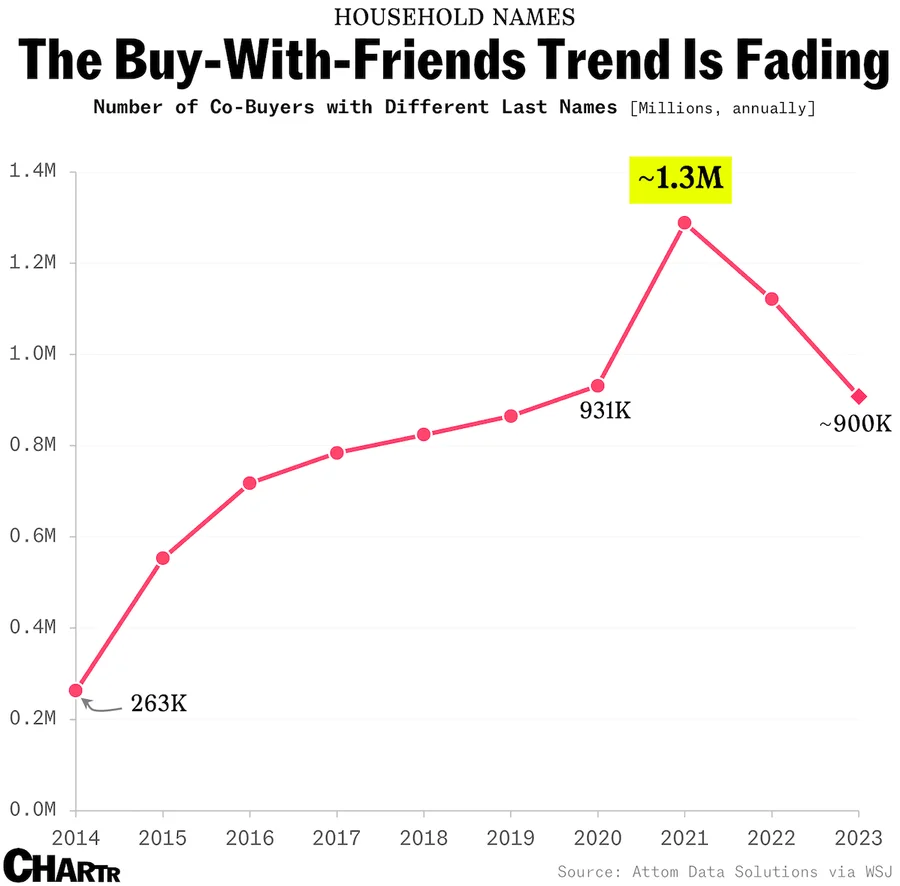

Why Co-Buying Took Off in 2023

Home prices surged, and interest rates hit highs not seen in decades. For many buyers, especially first-timers, splitting the down payment and monthly payment made homeownership possible when it otherwise wasn't. Co-buying wasn't just convenient. It was often the only path in.

But co-owning with a friend has real complications beyond the finances. You're making long-term decisions together about a major asset: maintenance, refinancing, selling, what happens if one of you wants out. None of that is simple. As the market shifts, some of those arrangements are getting a second look.

How the Fed's Rate Cut Changes the Calculation

The Federal Reserve cut rates from 5.25%–5.5% to 4.75%–5%, and that move has real consequences for buyers. Lower rates mean smaller monthly payments and more people qualifying on their own income. A pre-approval that wasn't achievable at 7.5% might be well within reach at 6.5%.

More buyers are discovering they don't need a co-buyer to qualify for the home they want. As rates continue to fall, that trend will likely accelerate.

Wondering What You Qualify for on Your Own?

A quick conversation with our team can tell you exactly where you stand and what rate cut scenarios mean for your purchasing power.

What If You're Already Co-Owning with a Friend?

This shift can create difficult conversations. With more affordable mortgage options now available, one co-owner might decide they're ready to buy their own place, which can leave the other in a real bind. A buyout, a sale, or a refinance to remove one party from the loan: all of those options carry costs and require agreement.

The time to have that conversation is before rates drop far enough that one party is actively motivated to move on. Knowing your exit options in advance prevents a lot of friction down the road. Our guide to qualifying based on your own debt-to-income ratio is a good place to start understanding where you stand individually.

Should You Buy Solo or Co-Buy Right Now?

Co-buying still makes sense in some situations. High-cost markets, specific income constraints, or building a rental property with a partner, these are legitimate reasons to co-own. But with mortgage rates declining, it's worth running the solo numbers first before committing to a shared arrangement.

A loan officer can tell you in one conversation what you'd qualify for alone, and what the difference in monthly payment actually looks like compared to splitting costs. That conversation is free, and it gives you the information you need to make the right call.