You've found your dream home in Florida. Maybe it's a beachfront condo in Miami or a sprawling estate in Orlando. The catch: the price tag is higher than what most mortgages cover. That's where a jumbo loan comes in. Here's what these loans are, who they're for, and how to figure out if one fits your situation.

Jumbo Loans 101: How They Work in Florida

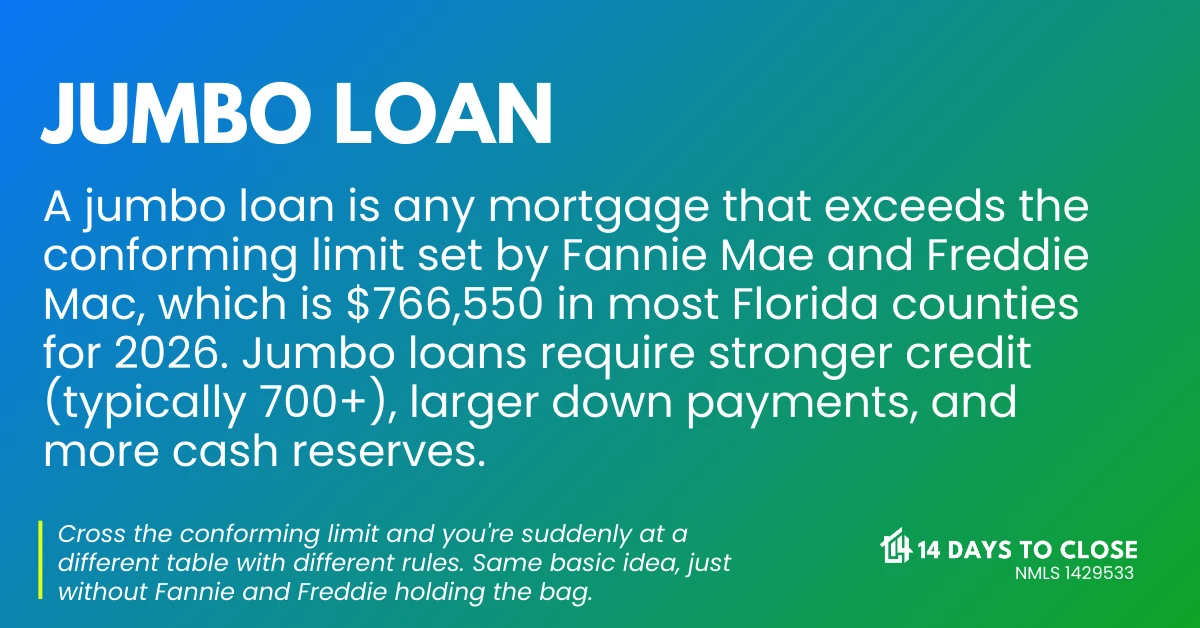

A jumbo loan is simply a mortgage that's too large to qualify for a conventional loan. Every year, the Federal Housing Finance Agency (FHFA) sets a limit on how much you can borrow with a conventional mortgage. In Florida, that limit for 2025 is $806,500 in most areas and $967,150 in higher-cost spots like the Florida Keys (Monroe County). If your dream home costs more than that, a jumbo loan is your option.

Because these loans are larger and riskier for lenders, they come with stricter rules. Think of it like applying for a VIP membership: you'll need strong credit, a solid income, and a bigger down payment to qualify.

Jumbo Loans vs. Regular Mortgages

Regular mortgages are backed by government agencies, which means lenders carry less risk. That's why they're easier to qualify for, even if your credit score isn't perfect or you can only put down 3 to 5%.

Jumbo loans are different. Since they're not government-backed, lenders want extra assurance you can pay them back. You'll need a credit score of at least 720 (aim for 740 or higher for the best rates), proof of steady income, and a down payment of 10 to 20% or more. Lenders will also verify your savings to confirm you have enough cash remaining after closing.

Qualifying for a Jumbo Loan in Florida

Here's what lenders look for in 2025:

- Credit score: 720 or higher is the baseline. 740+ gets you better rates.

- Income documentation: Pay stubs, tax returns, and proof that your employment or business is stable.

- Debt-to-income ratio: Lenders want to see your monthly debts don't exceed 43% of your gross income.

- Savings cushion: Expect to show up to 12 months of mortgage payments saved after closing.

If you're self-employed, plan to provide additional paperwork, including two years of business tax returns. Our guide to debt-to-income ratios covers exactly what lenders measure and how to prepare.

Shopping for a Florida Home Over $800K?

We work with jumbo loan borrowers every week. A quick call can clarify exactly what you'll need to qualify before you make an offer.

The Upsides and Downsides of Jumbo Loans

Jumbo loans cover Florida homes that conventional mortgages can't reach. You also get flexible terms, including fixed or adjustable rates, and may qualify for a rate that rivals conventional financing in a competitive environment.

The tradeoff: strict credit and income requirements can slow some buyers down, and the larger down payment means more cash upfront. If rates drop later, refinancing a jumbo loan tends to be more involved than refinancing a conventional mortgage.

Is a Jumbo Loan Right for You in 2025?

If you're looking at a Florida home priced over $806,500, or over $967,150 in the Florida Keys, and your finances are strong, a jumbo loan could be the right fit. If you're right at that limit, a regular mortgage with private mortgage insurance (PMI) might save you money overall. Think long-term: in markets like Tampa or Naples, a jumbo loan can help you build equity faster as home values rise.

You can compare your options in our overview of conventional loans to see how the structures differ before you decide.

Here's Your Game Plan

Mortgage limits don't have to hold you back. Our Florida team walks through jumbo requirements, real numbers, and timelines every week. A quick call can clarify exactly what you'll need, and we're available nights and weekends.