Buying a home with bad credit is harder. That's not sugarcoating it. But harder isn't the same as impossible, and with the right strategies, homeownership is still within reach for buyers who don't have a pristine credit file. Here's what actually works.

Know Where You Stand First

Before anything else, pull your credit reports from all three bureaus: Equifax, Experian, and TransUnion. You're entitled to free reports at AnnualCreditReport.com. Look at your actual scores, but more importantly, look at what's dragging them down. Late payments, high balances, collections, and errors all affect your score in different ways, and fixing them requires different approaches.

Errors on credit reports are more common than most people realize. If something looks wrong, dispute it directly with the bureau. A removed error can move a score 20 to 40 points in some cases, which is meaningful when thresholds determine which loan programs you qualify for.

Work on the Score, Even If It Takes a Few Months

You don't need to rebuild your credit completely before buying. But even a small improvement can expand your options. Paying down revolving balances lowers your credit utilization ratio, which is one of the highest-weighted factors in your score. Doing it consistently, and making sure every due date gets met on time, moves the needle faster than most people expect.

Loan Programs That Work with Lower Scores

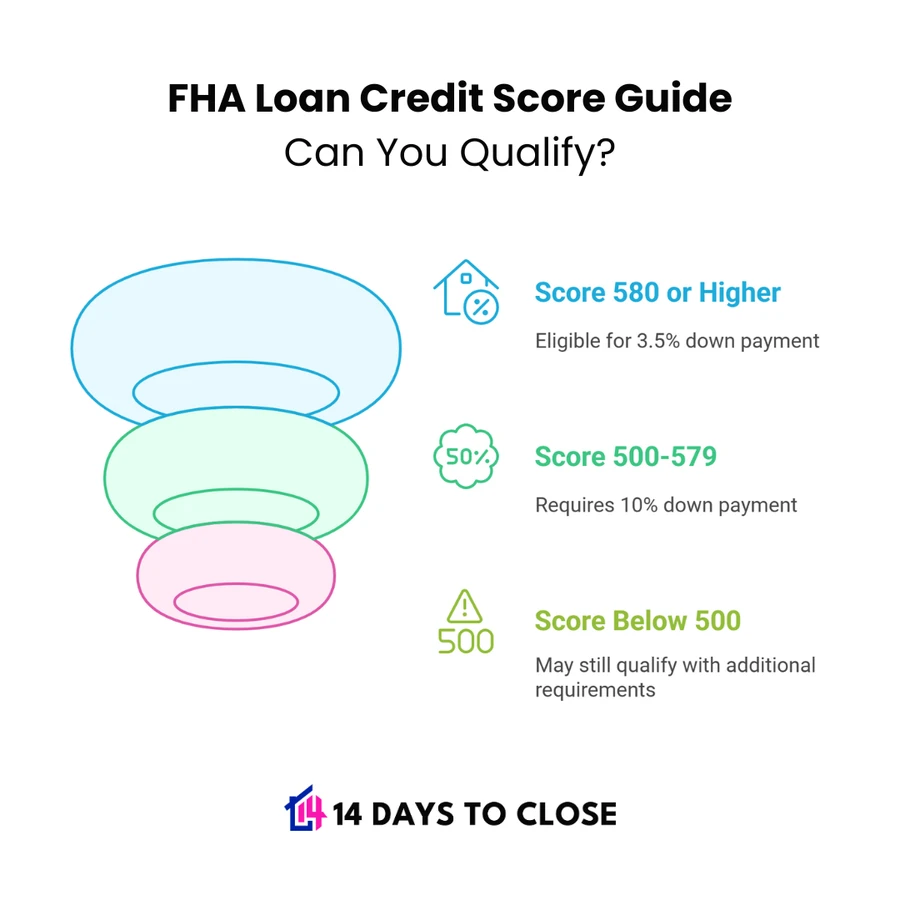

This is where things get practical. Not every loan program has the same credit floor. FHA loans, backed by the Federal Housing Administration, allow scores as low as 500 with a 10% down payment, or 580 for the 3.5% down option. That's a significantly lower bar than conventional financing, which typically requires 620 or higher.

VA loans, available to eligible veterans and active-duty service members, often have no official minimum score requirement. Individual lenders set their own overlays, but VA financing is generally more forgiving than conventional products. Comparing VA and FHA options is worth doing if you're eligible for both.

USDA loans serve buyers in eligible rural and suburban areas and also allow lower scores with some lenders, though requirements vary. If location works, it's worth asking about.

Get Pre-Approved Before You Search

Pre-approval isn't just for well-qualified buyers. Getting pre-approved with bad credit shows sellers you're serious and gives you a clear picture of what you can actually afford, including what your rate and payment will look like given your current profile. It also helps you identify exactly what needs to change if you need to wait and improve before buying.

A co-signer with stronger credit can also make a meaningful difference. Their income and credit history are factored into the application alongside yours, which can move you into a better approval tier. Make sure the co-signer understands the responsibility fully before agreeing.

Set Realistic Expectations About Cost

A lower credit score means a higher interest rate. That's just how lenders price risk. A 620 score getting a 7.5% rate versus a 760 score getting 6.5% adds real money to your monthly payment over 30 years. Use a mortgage calculator to run both scenarios so you know exactly what you're taking on. If the payment doesn't fit your budget, it's better to know that before you're under contract.

The path to homeownership with bad credit requires honesty about where you are, a plan for where you need to be, and a lender who's willing to work through the options with you rather than just declining and moving on. Buyers with 600 credit scores have closed loans with the right preparation and the right guidance.