FHA loan assumptions have been around for decades, but they became genuinely valuable when rates doubled in 2022. If a family member owns a home with a 2.75% or 3.5% FHA mortgage, you may be able to take over that loan exactly as it exists, keeping their rate, their remaining balance, and their original terms. No refinancing. No new underwriting at current rates. You step in and they step out.

It's not automatic, and it's not available on every loan. But when it works, the savings are real.

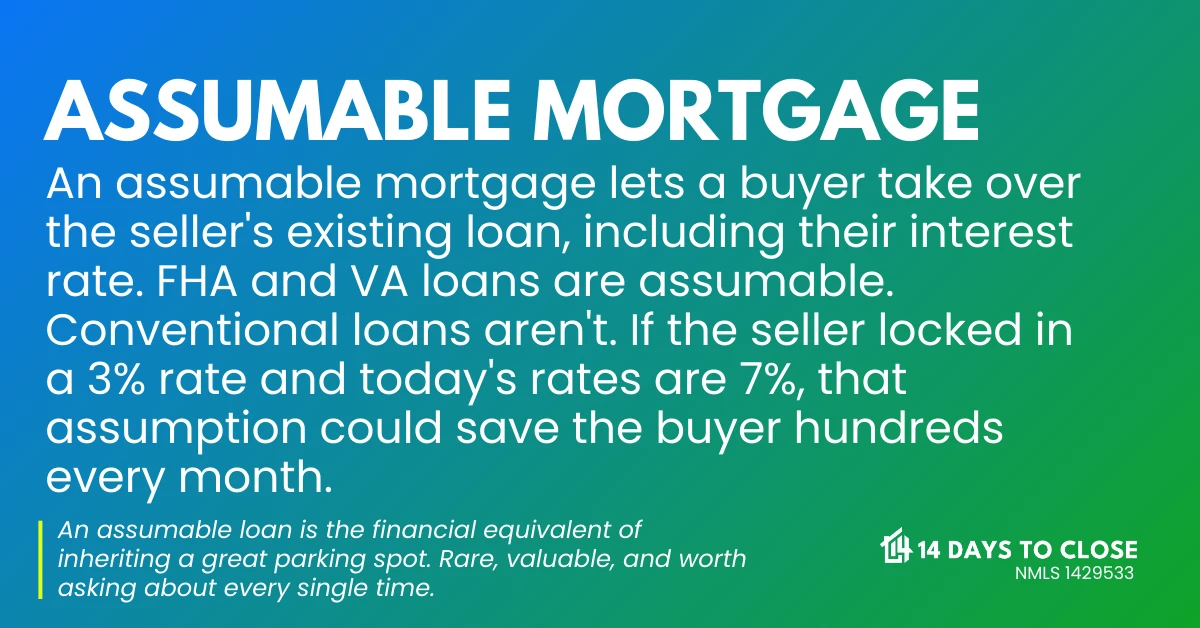

What Is an FHA Loan Assumption?

An FHA loan assumption means you take over an existing FHA mortgage from the current borrower. You assume the remaining balance, the interest rate, and the remaining term. The lender must approve the assumption, and you'll need to qualify as a borrower. But if approved, you're not getting a new loan at today's rates. You're inheriting the old one.

FHA loan assumptions come up most often during estate transfers when a home is inherited, during divorce when one spouse keeps the house, and in family real estate transfers where a parent or sibling wants to pass property to a relative.

The numbers are growing. FHA mortgage assumptions jumped from roughly 2,550 in 2021 to over 4,000 in 2023 as buyers recognized the value of inheriting pre-rate-hike loans.

Why You'd Want to Assume an FHA Mortgage

The math is simple. If the existing FHA loan is at 3.25% and current rates are 7%, assuming the old loan saves hundreds of dollars a month on the same balance. Over 30 years, that compounds into a significant amount.

Other reasons to consider assumption:

- Keeping a family property without refinancing into a new loan

- Divorce: one spouse keeps the home and removes the other from the mortgage

- Helping a family member avoid foreclosure by taking over their payments

- Avoiding the higher closing costs of originating a brand new mortgage

Can You Assume Any FHA Mortgage?

Not every FHA loan is assumable automatically. Three things need to be true:

- The loan must be FHA-insured. Conventional loans generally are not assumable.

- The lender must approve the assumption. You apply like a borrower, the lender reviews your credit and income.

- The existing mortgage must be in good standing. No active late payments or default.

If all three conditions are met, the assumption is possible. If the loan has been modified or the lender has restrictions built into the servicing agreement, it may be more complicated.

Steps to Assume an FHA Mortgage From a Family Member

- Confirm the loan is assumable. Pull the original note or contact the servicer directly and ask if the loan is FHA-insured and assumption-eligible.

- Qualify with the current lender. You'll go through a credit check (typically 580+ for FHA), income verification, and a debt-to-income review. Plan for this to take 45-90 days.

- Submit the assumption application. The lender will provide the paperwork. Include tax returns, pay stubs, bank statements, and any documentation relevant to the relationship with the current borrower.

- Pay the assumption fee. Usually lower than new loan closing costs, typically a few hundred to a couple thousand dollars depending on the lender.

- Complete the title transfer. Once approved, you officially take over the mortgage and the title transfers to your name. The original borrower is released from the debt (pending lender approval of the release).

What to Know Before You Start

Mortgage insurance stays. FHA loans carry monthly mortgage insurance premium (MIP), and it continues after assumption. This doesn't change with the assumption.

It takes time. Assumption applications can take 45-90 days or longer. Plan accordingly if there's a timeline involved.

The lender controls the process. The servicer may have internal procedures and timelines you can't accelerate much. Start early.

Release of liability matters. Make sure the original borrower gets a formal release of liability from the lender once the assumption closes. Without it, they're still technically on the hook if you default.

If someone in your family has a low-rate FHA mortgage and there's a reason to transfer ownership, this is worth exploring before assuming you need a new loan. We can help you review the existing loan documents, check assumption eligibility, and walk through the qualification steps. Reach out below to start the conversation.