Visual Breakdown

What's Inside a Typical Mortgage Payment

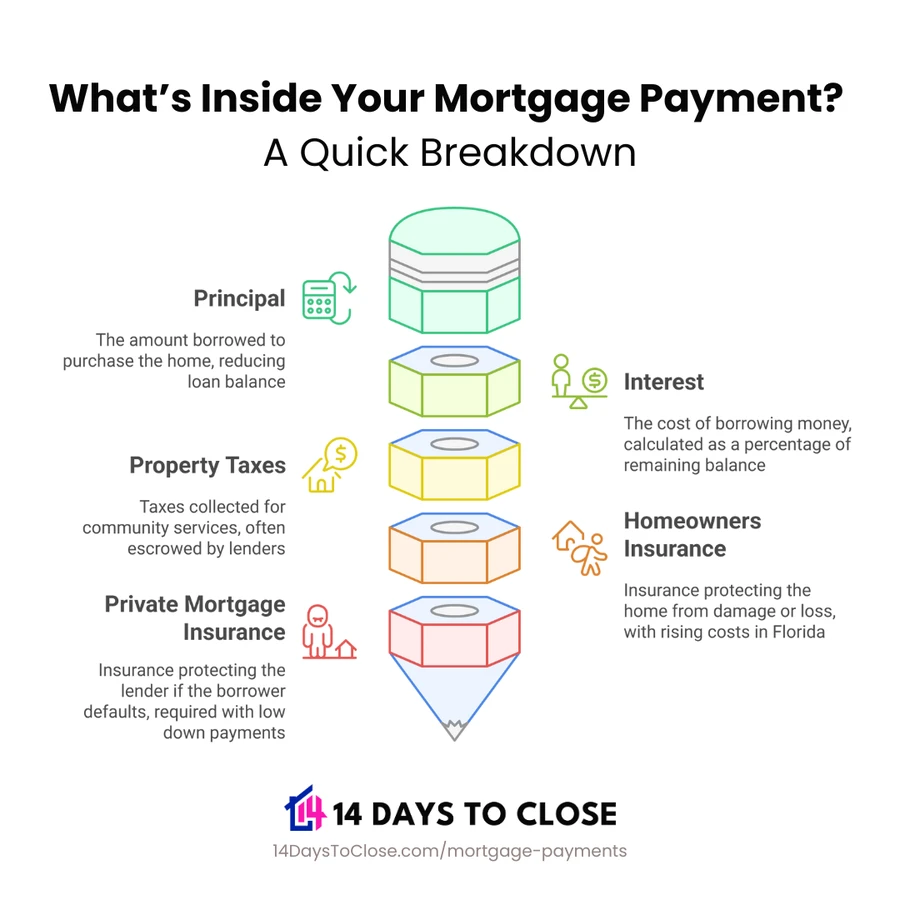

This infographic shows how the four payment components add up and how the split between principal and interest shifts over the life of the loan.

Most first-time buyers focus on the interest rate. The monthly payment surprises them. That's because a mortgage payment includes principal, interest, taxes, and insurance , the full PITI picture. Here's how each one works and what you can actually control.

Your monthly payment includes:

A 7% mortgage rate on a $300,000 loan works out to about $1,996 per month in principal and interest. But most buyers aren't paying $1,996. They're paying $2,400 or more. The difference is taxes and insurance.

In Florida, property taxes vary significantly by county. Homeowner's insurance , especially with recent premium increases , can add $200 to $400 per month to a typical payment. If you're putting less than 20% down, private mortgage insurance (PMI) adds another $100 to $250.

Understanding each piece of your payment before you're under contract helps you shop for the right price range and avoid the surprise of a higher-than-expected monthly obligation. Here's what goes into it.

Principal is the portion of your payment that reduces your loan balance. At the start of a 30-year mortgage, most of your payment goes to interest , not principal. That ratio shifts over time. By the end of the loan, almost all of your payment is reducing the balance.

On a $300,000 loan at 7%, about $246 of your first monthly payment goes to principal. That number increases each month as the loan amortizes. On a 15-year loan, principal paydown happens much faster , but the monthly payment is higher.

Interest is what the lender charges for the loan. It's expressed as an annual rate , but you pay it monthly. On a fixed-rate mortgage, the rate doesn't change. On an adjustable-rate mortgage (ARM), the rate resets after an initial fixed period.

The rate you get depends on your credit score, loan type, down payment, loan term, and market conditions when you lock. A 0.5% difference in rate on a $350,000 loan is roughly $100 per month , or about $36,000 over 30 years. The rate matters.

Florida property taxes are assessed by county and paid annually , but most lenders collect them monthly as part of your escrow account, then pay the bill on your behalf when it's due. The rate varies widely by county and property value.

Florida's homestead exemption reduces the taxable value of your primary residence by up to $50,000, which can meaningfully lower your annual tax bill. New buyers should note that the assessed value often jumps in the first year after purchase if the previous owner benefited from the Save Our Homes cap.

Your payment typically includes two insurance components: homeowner's insurance (required by all lenders) and, if you're putting less than 20% down, private mortgage insurance (PMI).

Florida homeowner's insurance has been volatile. Coastal properties and homes with older roofs often carry higher premiums. Getting an insurance quote before going under contract is smart , it affects your total payment calculation. PMI on a conventional loan typically runs 0.5% to 1.5% of the loan amount annually and can be removed once you reach 20% equity.

This infographic shows how the four payment components add up and how the split between principal and interest shifts over the life of the loan.

Start a pre-approval and we'll give you a real payment estimate , including taxes, insurance, and PMI , based on your actual loan amount and credit profile.

Some of these you control before you buy. Others become available after you close. All of them are worth knowing before you make any decisions.

A larger down payment reduces the loan amount, which reduces both principal/interest and any PMI requirement. It's the most direct lever for lowering your monthly payment , though it requires more cash upfront. If you're weighing a 5% down vs. 10% down scenario, the payment difference is meaningful.

Credit score directly affects your interest rate. A borrower at 760 typically gets a significantly better rate than a borrower at 680. Even a small improvement before applying can translate to a meaningfully lower payment over 30 years. If you're on the edge of a credit tier, spending 60 to 90 days improving your score is often worth it. See how credit scores affect mortgage rates.

Homeowner's insurance is required by your lender, but you choose the provider. In Florida, premiums vary widely between carriers. Getting two or three quotes before closing can reduce your escrow payment. Your lender will collect whatever premium you've arranged, so coming in with a lower quote saves you money every month.

If you're paying PMI on a conventional loan, you can request cancellation once your loan balance drops to 80% of the home's original value. If your home has appreciated, you can order a new appraisal to reach 80% LTV sooner. This move eliminates $100 to $250 per month for many borrowers.

If rates drop after you close, refinancing can lower your monthly payment significantly. A refinance replaces your existing loan with a new one at current market rates. The decision depends on how long you plan to stay in the home and the cost to refinance. Learn more about when refinancing makes sense.

You don't have to refinance to pay down your loan faster. A few simple changes to how you pay can cut years off your loan term and save thousands in interest.

Biweekly payments. Instead of making 12 monthly payments per year, you make half a payment every two weeks. Since there are 52 weeks in a year, that equals 26 half-payments , or 13 full payments. The extra payment goes straight to principal. On a 30-year loan, this strategy can shave 4 to 6 years off your timeline and save tens of thousands in interest. See the full breakdown on biweekly payments.

Extra principal payments. Any payment above your required monthly amount goes directly to your principal balance if you designate it that way. Even an extra $100 a month makes a meaningful difference over time. Tax refunds, bonuses, or windfalls applied to the loan balance can shave years off your term.

Rounding up. If your payment is $2,120, pay $2,200. The extra $80 per month goes toward principal and compounds over time. It's one of the simplest strategies and requires no formal setup with your lender.

A pre-approval tells you your rate, loan amount, and full payment estimate including taxes and insurance. Start here and shop with a real number.